법인소유 생명보험

Peter Lee - Dec 07, 2023

회사가 주주를 피보험자(Life Insured)로 생명보험에 가입할 경우...

이효석 (Peter Lee), MBA, CLU, CHS

Chartered Life Underwriter | Certified Health Insurance Specialist

CELL: 778-875-9328(BC), 403-875-9328(AB)

Email: Peter@meeraefinancial.com Website: www.meeraefinancial.com

Chartered Life Underwriter | Certified Health Insurance Specialist

CELL: 778-875-9328(BC), 403-875-9328(AB)

Email: Peter@meeraefinancial.com Website: www.meeraefinancial.com

법인(Corporate)이 주주(Shareholder)를 피보험자(Life Insured)로 생명보험(Life insurance)에 가입할 경우 생명보험 사망보험금(Death benefit)이 법인에 지급되면 자본배당계정(Capital Dividend Account, 이하 CDA)을 사용하여 보험금의 전부 또는 일부를 캐나다 거주 주주에게 비과세(Tax-free) 방식으로 분배할 수 있습니다.

- 생명보험 사망보험금 사용 용도:

(1) Funding a buy/sell agreement 주주 또는 파트너 Buyout Agreement 자금 조달

(2) Debt coverage for a business line of credit or loan 비즈니스 신용 한도 또는 대출

에 대한 담보

(3) Estate planning, including funding shareholder’s tax liability in death 주주 사망시

주주의 세금 납부를 위한 자금조달과 유산상속 플랜

(2) Debt coverage for a business line of credit or loan 비즈니스 신용 한도 또는 대출

에 대한 담보

(3) Estate planning, including funding shareholder’s tax liability in death 주주 사망시

주주의 세금 납부를 위한 자금조달과 유산상속 플랜

- 자본배당계정(Capital Dividend Account, CDA)

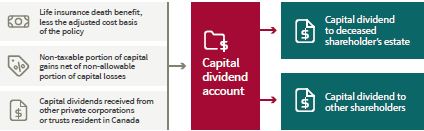

CDA는 캐나다에 거주하는 개인 법인(Private corporation)이 벌어들인 특정 유형의 소득을 추적하는 명목상 세금계정(Notional tax account)입니다. 예를 들어 법인이 실현한 자본 이득(Capital gain)의 비과세 부분(Non-taxable portion)과 생명보험 사망 보험금은 법인의 CDA에 적립됩니다. 법인의 CDA는 자본 배당금(Capital dividends) 형태로 자금을 비과세로 분배할 수 있기 때문에 캐나다에 거주하는 개인 법인의 주주에게 특히 유용합니다.

What determines a capital dividend account balance?

What determines a capital dividend account balance?

- 생명 보험과 자본배당(Capital dividends)

법인이 생명보험을 소유하고 있는 경우, 일반적으로 세금상의 이유로 법인이 보험의 수혜자(Beneficiary)가 됩니다. 피보험자가 사망하면 법인은 사망 보험금을 수령하며, 일반적으로 사망 보험금에서 보험의 조정된비용(Adjusted cost basis)을 공제한 금액만큼 CDA에 적립됩니다. 또한 생명보험이 법인의 부채를 담보하기 위해 사용되는 경우, 사망 보험금이 채권자에게 직접 지급되는 경우에도 법인은 동일한 기준으로 CDA에 크레딧을 받습니다.

자본배당은 법인이 특별 세금 양식을 사용하여 배당금을 자본배당으로 처리하도록 선택하여 지급하며, 선택 과정에는 세법에 대한 자세한 지식이 필요하므로 법인의 회계사가 참여하는 것이 좋습니다.

기업은 자본 배당금 지급 시기를 유연하게 결정할 수 있으나, CDA는 후속 거래의 영향을 받을 수 있으므로 가능한 한 빠른 시일 내에 자본 배당을 지급하는 것이 좋습니다. 예를 들어, 사망 보험금을 수령한 후 법인이 실현한 자본 손실에 따라 CDA가 감소할 수 있습니다.

감사합니다

Disclosures

The information provided is based on current laws, regulations, and other rules applicable to Canadian residents. It is accurate to the best of our knowledge as of the date of publication (January 2021). Rules and their interpretation may change, affecting the accuracy of the information. The information provided is general in nature and should not be relied upon as a substitute for advice in any specific situation. For specific situations, advice should be obtained from the appropriate legal, accounting, tax, or other professional advisors.